General Discussion

Related: Editorials & Other Articles, Issue Forums, Alliance Forums, Region ForumsGet ready for insurance sticker shock in 2014

I resigned my current job last week, with the idea that I was going to try to work on my own. I figured I'd COBRA my health insurance until Jan.1, and then sign up for an ACA plan.

Well, since I haven't been able to log in to the Exchange since it opened (my latest problem is being kicked right back to the login screen as soon as I click 'Login'), I thought I'd go to the Anthem site and see what they were quoting policies at.

The first thing you have to do is say what year you want the coverage for. I thought I'd try both 2013 & 2014 and see what came up.

Well, was I ever shocked!!! A policy for both my wife & myself (we're 58/59 yrs) came up for about $380/mo for 2013, but ***$800*** a month in 2014!!!! What the???

I did a Google search about 2014 rates, and it seems like insurers agree that rates are going to skyrocket next year

Needless to say, I'm not feeling real good about quitting my job with its coverage right now...

Interestingly, when I went to the healthcare.gov page that gives estimated plan costs, the figures shown there were more in line with the 2013 rates. Is that a problem, or is there something I'm not taking into account?

We're not eligible for subsidies, either - we're just outside the income range.

I hope all the people who've posted here about the good deals with the ACA aren't going to have a rude awakening when the bills start coming in next year

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

= new reply since forum marked as read

Highlight:

NoneDon't highlight anything

5 newestHighlight 5 most recent replies

arcane1

(38,613 posts)Sorry, I'm on my phone right now & can't figure out how to link.

If you Google 'Bloomberg Aetna insurance 2014' you'll get an article on Bloomberg.

Although, the Aetna CEO's opinion is debated by others at the link. All I know is the Anthem site shows a big difference between 2013 and 2014 rates.

Pretzel_Warrior

(8,361 posts)notadmblnd

(23,720 posts)Welcome to DU, but if you expect your visits to be pleasant it is a good idea to back up what you say with proof.

JoePhilly

(27,787 posts)Pretzel_Warrior

(8,361 posts)I think this is a bullshit hypothetical written by some caver or other troll.

anneboleyn

(5,611 posts)to just "try" working on his own w/out expecting a nasty wake-up with respect to insurance costs and everything else? With retirement and the most crucial years in terms of healthcare just ahead? No sane person would do something so reckless, and then write up a post for DU acting as though this is all the fault of "evil Obamacare." I am REALLY tired of these posts. I agree with you Pretzel_Warrior. Trolls.

Response to bcool (Original post)

lostincalifornia This message was self-deleted by its author.

SoCalDem

(103,856 posts)It was set up to provide insurance (often for the FIRST time) to people who could not get it through a job or on their own dime...and for people who had been denied coverage before.

Phase TWO of the ACA will probably be to gradually turn this into single payer as large companies start to wean their employees off company provided plans.

For many people, there may be some "adjusting" necessary to make it all financially easier. For instance, if the family income is too high (but close), perhaps a few hundred less in paycheck each month (reduced hours worked) could translate into a win-win, if you would then qualify for a greatly reduced insurance bill

The sad fact is that for people who already HAVE insurance that is deemed "affordable", the ACA was never going to be a bargain....and for people with "middle" incomes, and who were in the 40-64 age groups, it's costly.

It's mostly to get more people to qualify for medicaid, for youngish folks who went without because they had low incomes, and for the formerly uninsurable

Response to SoCalDem (Reply #43)

lostincalifornia This message was self-deleted by its author.

frazzled

(18,402 posts)If you don't want to buy insurance on the exchanges, you will be of course be at the mercy of private insurers.

The point of the exchanges is to buy into POOL rates, not individual rates.

Pretzel_Warrior

(8,361 posts)not

Demo_Chris

(6,234 posts)Pretzel_Warrior

(8,361 posts)

ScreamingMeemie

(68,918 posts)And, I posted proof:

WilliamPitt

(58,179 posts)alcibiades_mystery

(36,437 posts)Whew. I think I may be coming down with a cold.

JoePhilly

(27,787 posts)

Tarheel_Dem

(31,234 posts)

dionysus

(26,467 posts)PUT UP YER DUKES!1!

Tarheel_Dem

(31,234 posts)

dionysus

(26,467 posts) karate choppin!

kick boxin!

kick boxin!

Tarheel_Dem

(31,234 posts)

dionysus

(26,467 posts)

Tarheel_Dem

(31,234 posts)

tallahasseedem

(6,716 posts)this cold will be spreading through DU pretty quickly over the next couple of months!

Arugula Latte

(50,566 posts)

NightWatcher

(39,343 posts)COBRA costs a fortune and buying a policy for two people from an insurer with no employer help is crazy right now.

Why didn't you wait till you knew the prices?

Forget it, you're probably full of it anywhoo.

Scuba

(53,475 posts)BlueStreak

(8,377 posts)for pointing this out. We don't cotton to folks using that kind of loose talk around these here parts.

But you have stumbled onto a huge problem. The insurance companies have been very quiet the past year because they knew effective 1/1/2014, they had the biggest opportunity in their histories:

1) The law requires millions of people to enroll

2) The government will be paying for most of it

3) Insurers are required to make some significant changes to their risk profile - therefore no possibility for apples-to-apples

All of those things taken together spell MEANS, MOTIVE, and OPPORTUNITY.

To cut to the chase, this is a huge ripoff being perpetrated and it is going completely without notice because there are three other stories preempting it:

a) the govt shutdown, presumably including the furloughing of the people who would normally watch-dog this

b) the possible default

c) the horrendous clusterf%%% that was the launch of Healthcare.gov.

These guys are robbing the bank and nobody is even talking about it.

Yes, I am perfectly aware that the ACA puts a limit on overhear/profit. And anybody who trusts that they intend to honor that without massive trickery and cooking of the books is a complete fool. Yes, maybe 5 years from now, the next administration will win some judgements against these companies, but the crooks are willing to take their chances. If it is anything like the banking settlements, even a Democratic administration would just give them a gentle slap on the wrist and ask them to try not to do so much of that bad stuff in the future.

Pretzel_Warrior

(8,361 posts)BlueStreak

(8,377 posts)Perhaps some insights that others might consider helpful?

grantcart

(53,061 posts)OPM.

Your ignorance on how the system actually works is profound.

For example:

maybe 5 years from now, the next administration will win some judgements against these companies

They aren't judgments, they are automatic refunds, which started last year:

http://www.whitehouse.gov/blog/2013/07/18/refund-your-health-insurance-company-thank-affordable-care-act

Did you know that 8.5 million Americans are getting a refund this year from their health insurance companies?

Thanks to a provision in the Affordable Care Act, if your insurance company isn’t spending at least 80 percent of your premium dollars on medical care, they have to send you some money back.

Today in the East Room, President Obama explained that “last year, millions of Americans opened letters from their insurance companies -- but instead of the usual dread that comes from getting a bill they were pleasantly surprised with a check. In 2012, 13 million rebates went out, in all 50 states." Another 8.5 million rebates are being sent out this summer, averaging around $100 each, he said.

Over 10 million people have already received $ 1.5 billion in refunds.

More to your general point: The plans are good, but now they have a level field with MLR and market access. If any company tries to over charge they aren't going to get any business.

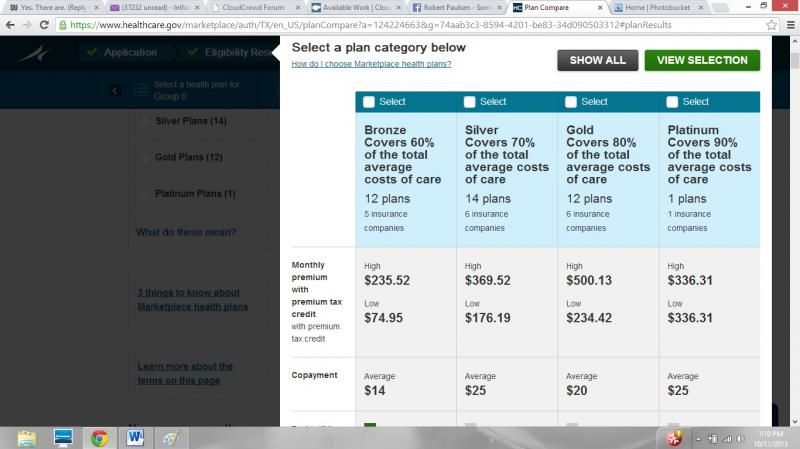

I qualified for 110 plans. I only looked at the cheapest 5 Gold plans.

BlueStreak

(8,377 posts)If so, you are insane. These companies do every sleazy thing they can get away with, and what we are seeing now is essentially a jailbreak. They know that Obama can't go after them because: 1) they are all breaking loose, so there just aren't enough resources to run them all down. And 2) Obama NEEDS them. They know it and he knows it. He needs all of them in the exchanges so that he can declare victory.

And what the hell does Obama care if they are running up the prices? The government is paying for all that anyway. The Obama administration's only focus is going to be to try to get people enrolled in these grossly overpriced policies, and maybe they will worry about the price gouging later -- or maybe not.

To recycle a quote, your ignorance about how large corporations operate is profound.

grantcart

(53,061 posts)1) First you argue that the MLR will only account in refunds 5 years down the road which even people with only a superficial knowledge with the ACA.

The refunds that you said would happen in the future, happened last year,

http://abcnews.go.com/Politics/obamacare-health-insurance-rebates-check/story?id=19701785

An estimated 8.5 million Americans will receive rebates from their health insurers this summer thanks to the Affordable Care Act, which says companies that fail to spend at least 80 percent of premiums on health care must refund the difference to consumers.

2) Having served as a CEO of medium sized corporation (400 employees) I have a very good familiarity with exactly how large corporations maintain their financial records. Corporations have to bring in outside auditing firms to conduct extensive checks on their accounting systems. While there have been a few cases of large corporations conducting false accounting practices (like Enron) they have been short lived and resulted in criminal prosecution.

The methods and standards used by the auditors are rigorously controlled and if they fail to follow them, and they are very thorough then they would lose their reputation (i.e PriceWaterhouse collapse) but also become personally liable for shareholders loss and criminal prosecution.

3) You seem to think that there is some incentive for executives to conspire to DECREASE profits. This is really rather humorous. When there have been criminal schemes to defraud it wasn't to conceal profits but to try and establish profits where they didn't exist (so that share price and executive bonuses would be increased).

So what you are arguing is that these executives would engage in complicated conspiracies involving hundreds of people and expose them to civil and criminal prosecution to hide profits and depress share price which would negatively impact their own share value and calculation of executive bonuses.

So when I used the word profound I was being polite, you have no idea of what you are talking about. But as John LeCarre once remarked by one of his characters "he was someone who was so fed up and couldn't take it any more that in his anger he lined up for a second helping".

You have exhausted my time limit on wild ass rants without factual understanding of which they talk about so I cede you the last and final word:

Please proceed.

BlueStreak

(8,377 posts)Companies do what they can get away with, period. The climate was not conducive for cheating on the rebates in 2013 because they knew a much bigger payday awaited starting 1/1/2013.

You seem to have quite a high estimation of your business accumen, and then say things that belie that. I would just caution that many people here have experience in all fields in all sizes of corporations. The knowledge your are presenting hardly sets you apart.

JustABozoOnThisBus

(23,350 posts)It'll be the death of us all!

onethatcares

(16,169 posts)six years ago after she lost her job and our healthcare insurance. Our premiums with COBRA/Aetna were $865.00 per month. So I don't see that big a shock.

My concern is: What do healthcare insurance companies add to the mix except another layer of profit margin?

Yo_Mama

(8,303 posts)That is the link. It will show you all the plans and prices on the exchange for your area. Pick the ones that interest you and then go to the individual insurer(s) to get accurate information (the age rating will change prices).

If you are not going to get a subsidy you do not need to go through all the hassle of the exchange. But if next year's income is significantly lower than this year's because you do not have a job, you may qualify for the subsidy and therefore want to apply through the exchange.

ACA coverage without subsidies is significantly more costly than pre-ACA coverage, that is true. But still you need insurance. You may also get a more limited plan from an insurance company that does not have all the coverages. If the premiums of all the ACA plans available to you are more than 8% of your income, you will not have to pay the penalty.

Best of luck.

bcool

(219 posts)I went back and looked at the estimates on healthcare.gov and noticed they didn't ask my age. Hmm..how can they provide an accurate estimate without that, since the premiums vary with age?

So, I went back to Anthem and got a new quote using ages 28/29 instead of our 58/59....and they came out almost exactly to those at healthcare.gov.

So, beware, the estimates may not be what you'll actually get when you provide your full information.

Yo_Mama

(8,303 posts)But going through the government exchange guarantees (or should, if it is working right) that the person sees all the insurance companies offering ACA policies.

Then you look at the ones that are of interest and check them out at the insurance site, which will be accurate.

The healthcare.gov tool only ask whether you are under or over 50, which will distort pricing.

People who are not getting subsidies anyway have no need to go through the exchange hassle.

Pretzel_Warrior

(8,361 posts)

TeamPooka

(24,229 posts)because that is the language of "professional posters".

buh bye now.

zappaman

(20,606 posts) dionysus

(26,467 posts)

CatWoman

(79,302 posts)i bought some peaches and left them in the car.

Drew Richards

(1,558 posts)For starters you are quoting an insurance execs preditions on the coming year and then claim anthem is raising rates... The 2014 price you quoted sounds like anthems typical family price as it currently is....from $800-1500 dollars..so there is no change in anthems current gouging price...

Then you really stick your foot in mouth and claim rates may...may go up foreverybody and claim as proof your undocumented quote from ACA.

But if...you actually quit your job and are starting an independent business you will have no or a low income projected for next year meaning you WOULD be eligable for subsidies unless you are gojng to claim you will go from unemployment to 68+K in the next 12 months...

So again, i cant understand you, are you confused and asking for help figuring out your true ACA cost...or are you just fear mongoring through ignorance or intent?

By the way if you want a true ACA estimate try going here plug in you basic info and get back to us...

Www.valuepenguin.com

Drew Richards

(1,558 posts)Bunnahabhain

(857 posts)You and your wife are 58/59 and you quit your job to start your own business with all kinds of important expense variables completely unknown to you. So here's my stab:

Your new small business is not in strategic planning and consulting.

ecstatic

(32,707 posts)First of all, it's always a bad idea to quit without a backup plan, because you basically forfeit your ability to collect unemployment insurance.

Secondly, how are you outside the income range if you're unemployed? Or does your wife still have a high paying job, which means you likely have access to employer group insurance?

Gravitycollapse

(8,155 posts)

PasadenaTrudy

(3,998 posts)troll troll troll...

hunter

(38,317 posts)My wife and I have run COBRAS out to the bitter end. We've been uninsured and uninsurable. Our medical problems are the consequence of random shit that could happen to ANYONE. We don't smoke, we eat good food, we get good exercise, we take care of ourselves, we wear our setbelts, and we don't have dangerous hobbies.

Our current medical insurance is through my wife's work. Our current medical expenses are high (insurance + uncovered = $16,000 or more annually, sometimes much more than that) but I find it a great comfort that with ACA we will not be uninsured and uninsurable again. Maybe someday we'll have a credit rating again too, and no collection agencies calling about medical debts. (I'm currently avoiding my own doctor once again because I owe him money. He'd probably see me anyways, we go back a long ways, and insurance has paid most of his fees but I still feel bad.... Primary care physicians put up with a lot of crap and work hard for the money.)

There will be problems with ACA. I hope you can afford your COBRA and that ACA will pleasantly surprise you when you are able to climb on board.

I find it comforting that my wife and I will no longer be excluded for "pre-existing conditions." And if we are not making money, like maybe because we are too sick to work, then the coverage will be subsidized.

A single payer health system would be best, but the ACA is better than what we had before.

AlinPA

(15,071 posts)Cross-Blue shield and it is going up by only $2 per month next year. I'm retired on Medicare.

scheming daemons

(25,487 posts)Cool story, bro

CatWoman

(79,302 posts)this is a most entertaining thread

kentuck

(111,101 posts)Before you even checked out the prices?? Wow!

ChazII

(6,205 posts)I don't know if this helps in any way. ASRS is the Arizona State Retirement System. Right now I am paying $715 but I hdo have other health issues and went with a more expensive plan but not the most expensive.