http://www.dailyreckoning.com/Issues/2008/DR082708.htmlAfter the biggest spending and borrowing binge in history, Americans need time and money. They need to pay their debts. They need to build savings for their retirements. They need time and money to recover from their mistakes.

What kind of mistakes?

Well, down near the bottom of the ladder, people bought houses they couldnt really afford to own in places they couldnt afford to live. And cars they couldnt afford to run. Those mistakes need to be undone. Which is why there are so many foreclosed houses on the market...and why house prices generally are falling.

S&P/Case-Shiller reports that house prices took their biggest hit ever in the second quarter of this year. They were down 15.4% from the year before.

Further up on the ladder, the rich are now embarrassed by their own housing mistakes. New Yorker magazine reports that it is the season of white elephants in Greenwich, Connecticut. Speculators began huge mansions in the Georgian Stockbroker style, for example, complete with indoor swimming pools, wine cellars, movie theatres, dozens of bathrooms, even ice-skating rinks and now find the buyers have disappeared. Want to buy a $28 million spec house? Go to Greenwich.

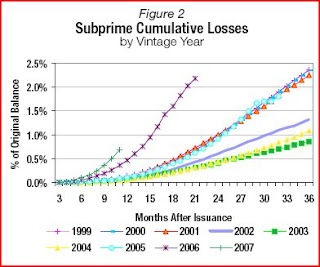

At the investment level there were plenty of mistakes too. Subprime mortgage lending dominated the headlines for the last 12 months, but the same reckless spirit found its way into transactions all over the economy. Private equity, IPOs, student loans, shopping malls, fast-food joints while the going was good, everyone wanted to go along.

And now, they all need time and money to pay for their errors.

The baby boomers say they are postponing retirement. Some are going back to the office.

A county in Alabama says it will have to declare bankruptcy.

The FDIC says its problem list of banks lengthened by 30% during the second quarter.

Bank earnings fell to their second lowest level in 19 years, says Bloomberg .

In London, tens of thousands of jobs have already been lost in the financial sector, says the Financial Times . IPOs, where the City (equivalent to Wall Street in New York) made much of its money, have fallen off a cliff.

We have lived through the biggest credit expansion ever. Ahead is perhaps the biggest credit contraction ever. Why? Because it takes time and money to correct mistakes. The bigger the mistakes; the longer and more expensive the correction.

Corrections can be tough on the economy and on the individual consumer. Most have no idea what lies ahead...but our friends at Strategic Investment have made some interesting forecasts. Read their latest report, which outlines not only the next 5 supershocks the U.S. economy should brace itself for, but how you can protect your portfolio and even turn a nice profit. See the report here .

When money and credit flow, they tend to raise prices. You get inflation first of asset prices...later, of consumer prices. When money stops flowing, prices come down. As George Soros puts it, the willingness to lend is directly related to the value of the collateral. Both tend to rise and fall together.

Currently, lenders are wary and the value of the collateral is falling. Everyone knows house prices are going down. But U.S. stock prices are going down too. Adjusted for consumer price inflation, theyve been going down since the end of 1999. That is, a $50 stock is still worth about $50...but the 50 bucks aint what it used to be. It buys only 1/5th as much oil, for example.

This trend, towards lower asset prices, is likely to last a long time. To protect ourselves, we began buying gold in 2000. So far...so good.

*** Gold hasnt done too well lately, maybe its time to get out...

The thought comes up from time to time, most recently from a visitor from Maryland.

If the world economy is slowing down, commodities arent the place to be, he went on. Gold either. People buy gold to protect themselves from inflation. But inflation isnt going to increase in a recession. Youd be better off in cash until this thing turns around.

Our guest voiced what is probably the dominant opinion of the summer that a worldwide slowdown means price increases will slow down too. Without the hot breath of the inflation hounds chasing it, gold will go back to sleep and the Fed can continue to rescue speculators from their mistakes.

Thats why the U.S. 10-year Treasury note yields all of 3.78%. Yes, investors know they will lose money if inflation remains above 4%. But that risk they believe is worth taking for the safety of the dollar and the full faith and credit of the U.S. Federal Government. Besides, inflation is almost sure to go down.

This view may turn out to be right. But when we think of moving to cash we pose the question: what cash? And theres the problem. The planets alpha cash is the dollar. And while the dollar may have some limited upside in a punk market (its already gone up about 7% against the euro), the potential downside is enormous.

What if the bond market is wrong about inflation? What if the increase in producer prices now running at nearly 10% works its way into consumer prices? What if demand from the developing world doesnt slack off as expected? What if there is war? What if the U.S. economy worsens...and the feds need to cut rates and offer further $100 billion bailouts? What if Asian, Arab and Russian creditors lose faith in the dollar and switch to euros?

Any of these things could be catastrophic for holders of U.S. Treasury bonds. At 3.78% yields it hardly seems worth the risk. Shorter-term Treasury bills barely pay anything at all.

So what cash do you hold? We choose gold because it is cash that no central bank manages. No one prints. No government backs. And no one ever threw away a gold coin. Gold will always hold an intrinsic value so well keep holding gold. And perhaps youll want to take out a golden insurance policy for your portfolio as well. See here:

Zero-Downside Gold

*** Colleague Joel Bowman of The Rude Awakening lives in Dubai. We wondered whether the place was the bubble we had heard, so we posed the question to him. His reply:

My short stay here in Dubai has led me to believe that Dubai & Co. is a largely unsustainable enterprise.

Dubais lifestyle makes the average American look like a prudent, energy-conscious, environmentally-friendly health nut! I read the other day that 60% of the average Emirates total income is spent on consumer goods Gucci totes, designer abayas and million-dollar number plates.

The big difference I can see is that, save for the last few years, the vast majority of Americas wealth accumulated over time and from the productive, honest toil of citizens who forged metal, cracked bullwhips and invented light bulbs. Dubais wealth has come on fast and strong...and is not really the product of its own honest toil. Were it not for American, British and French companies among others who told them what all that black stuff underfoot was and what the rest of the world was prepared to pay for it, Dubai might still be a pearl diving port of a few thousand itinerant workers.

If the American economy is drunk on its own home brew of irrational exuberance, Dubai is sucking down straight tequila shots and desperately trying to catch up. We see it here everyday as the government squanders its unearned wealth on extravagant welfare programs and National Identify Preservation boards and committees dedicated to cultural heritage association this and watchdog for immoral behaviour that. Then theres the over-reaching controls on the economy price fixing, wage manipulation, rent caps...the list goes on.

I read with interest the Frapp On Ice story just the other day about how Starbucks will close 600 stores over the next year as discretionary consumer spending shrinks. That story was all the more amusing for me as I actually read it on my laptop... in the Starbucks that just opened in the lobby of my building last week. There are now six Starbucks within walking distance from my front door (and I dont walk far it was 125 degrees on Monday). We also have numerous Seattles Best, Krispy Kremes and the rest of the strip mall junk to go along with them. Its like anytown USA...super-supersized. Which brings me to my next point...

Jumeirah Beach Residence (or JBR for the cool kids) is a 36-building project that opened a year or so ago. Each building is around 40 stories and there is said to be space for 25,000 people to live here. But where are the people, I ask myself? So few apartments are occupied that I still notice when a conspicuous new light comes on at night in the surrounding buildings...yet, apparently, most are sold. I cant see the newbies rushing to cut more keys as rent prices have, get this, risen by over 50% since we moved in in December. We took a relatively comfortable two-bedroom with a decent view, but if I walked in off the street today I couldnt get a studio on the first floor for the same price.

The story is similar elsewhere in the city too. Projects are developed, pumped through the massive Dubai & Co. media arm and, voila! the joint is 50, 60, or 70% taken! Its another success story, ring the papers Dubais world-beating ingenuity triumphs again! chorus the king and his merry band of sycophants. But, best as I can make out, the biggest developments including JBR, touted as the largest single-phase residential project in the world are still ghost towns.

A friend of mine was out the other day to inspect a house he saw for sale in one of these new developments (Arabian Ranches, in this case). The price was at the top-end of his budget and he was umming and ahhing about it until the estate agent casually threw in, now, this property is only available in lots of 10. In other words, the development is being sold off in 10-house chunks to middle-men who then flip em and burn onto the next world beating development.

So whos buying all these vacant houses, streets and islands? Some and not just the conspiracy theorists either say Dubai is a massive funnel for dirty Russian money. Others, including myself, reckon speculators buy into the hype...hoping a bigger idiot will buy into it a year later and hand them a handsome return.

The trouble is, sooner or later youre going to run out of idiots. Even here in Dububble the supply of them is not without limit.