The Truth about Option ARMs, Pick-a-Pay Mortgages, and Alt-A Loans: Looking at Wells Fargo, Bank of America, and JP Morgan. We are in the Eye of the $469 Billion Toxic Mortgage Hurricane and Silence is not Golden.

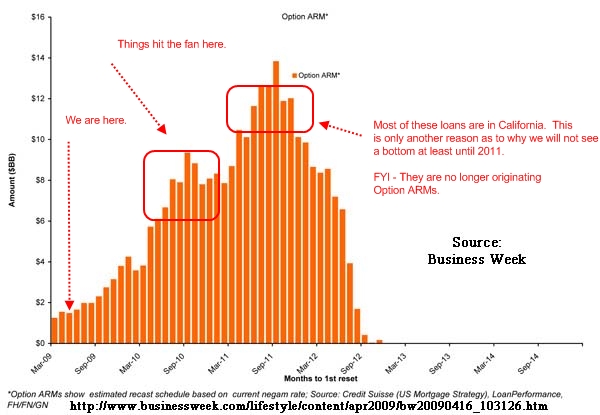

Let me be abundantly clear. We still have a Pay Option ARM and Alt-A mortgage problem. This will hit in full force in 2010 and we are already seeing many mortgage holders having trouble with actual recasts brought on by negative amortization. Yet there is a crew of people saying that Alt-A mortgage products will not bring any trouble because of the low interest rate environment. Unfortunately the low rate misses the bigger issue. Low rates are helping but the problem that we will be seeing is the massive onslaught of recasts, not resets that will be occurring over the next few years. This is a big reason why we wont see a housing bottom in California until 2011 at the earliest. Many of these loans were made to supposedly better qualified borrowers in mid to upper priced areas. These areas will begin to crack like an egg dropped on the floor late in 2009. The Notice of Default tsunami will guarantee this much.

Im am stunned that some people are actually saying that Alt-A mortgages or Pay Option ARMs will create little problems in the market. Okay. Then how about we remove the public-private investment program that conveniently has a cap with the FDIC of $500 billion? After all, if there isnt any problem with toxic mortgages why should we have a toxic mortgage program that has the design to eat up $1 trillion in loans. Exactly. Let me break down the latest figures from data by none other than the Federal Reserve:

http://www.doctorhousingbubble.com/the-truth-about-option-arms-pick-a-pay-mortgages-and-alt-a-loans-looking-at-wells-fargo-bank-of-america-and-jp-morgan-we-are-in-the-eye-of-the-469-billion-toxic-mortgage-hurricane-and-silence/